Interested in learning more about property mortgages in Canada? Look no further!

Latest News

Long-term mortgage rates are falling. Is it time to lock in? + MORE Apr 4th

Locking in or not depends on many factors, experts say, including whether the penalties for breaking a current mortgage make sense and if you think rates are going up or down..... More »

Latest in mortgage news: Borrowers must adapt to ‘new normal’ of higher rates, says Macklem + MORE Jun 17th

Interest rates may slowly start to be easing around the world, but they won't be returning to pandemic levels and borrowers will need to adjust accordingly..... More »

Making sense of the markets this week: September 24, 2023 + MORE Sep 23rd

Allan Small, Senior Investment Advisor at the Allan Small Financial Group with iA Private Wealth, shares financial headlines and offers context for Canadian investors.

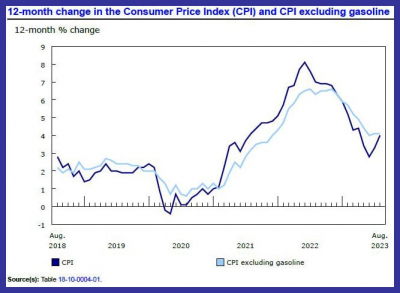

No surprise: Canada’s inflation rate ticked up in August

Canada’s annual inflation rate jumped to 4% in August, up from 3..... More »

Latest in mortgage news: bond yields plunge as U.S. inflation eases + MORE Nov 16th

Canadian bond yields took another step down today following the release of lower-than-expected inflation data south of the border..... More »

Why are mortgages so expensive in Canada? + MORE Nov 21st

Canada’s mortgage market has now absorbed four Bank of Canada (BoC) rate cuts, and house hunters are feeling the effects. The latest housing affordability data compiled by Ratehub.ca finds that lower mortgage rates made it easier to purchase a property in nearly every major Canadian housing marke.... More »

Less than 10 Percent of Canadians Could Buy a House in Toronto

– ratesupermarket.ca

Thinking about owning a home in Canada? It was only a few years ago that Toronto and Montreal were ranked among the best places to live with the cost of living as a contributing factor.

But the cost of ownership has now skyrocketed. In cities like Vancouver, Toronto and Montreal, only those in the highest income brackets can afford to live there. But there’s hope for potential homeowners. Widening your search can help you find affordable housing.

We used the RateSupermarket.ca mortgage affordability calculator to determine the household income brackets needed to own homes in each major city.

Cost of Owning a Home in Major Cities

A Zoocasa study found that Toronto’s benchmark house price is $873,100. Only those with income in the top 10 percent are able to afford homes there. Vancouver’s benchmark house price is $1,441,000 and only those in the top 1 percent can afford a home there.

Our Calculations

The lowest mortgage rate on RateSupermarket.ca is 2.75 percent but we used an average figure of 3…

Do You Need Loan Insurance?

– ratesupermarket.ca

Managing debt can be a challenge. Sometimes that challenge is driven by circumstances out of your control. Critical illness or disability can put a huge strain on your finances, making it hard to pay off a credit line or loan.

Those times of distress are what loan insurance is designed for. But is it always the right choice? Depending on the type of debt, your lender and your personal circumstances, it may be the best fit — or just another option.

How Does Loan Insurance Work?

Your lender may offer loan insurance at the time of application for a credit card, loan or line of credit. You’ll have to pay either a one-time, upfront fee for the policy, or a regular premium. Insurance might cover the remaining balance in the event of death, or regular payments while you are sidelined due to disability or serious illness. Some policies may also cover you in the event of job loss.

If you don’t sign up for insurance at the time of application, you may be able to do so later…

What to do with a monetary advance on your inheritance

– moneysense.ca

Q. My amazing parents are downsizing and have decided to gift my husband and me $200,000. It’s nice for us but leaves me with a lot of questions. My husband and I are 37 years old and have been happily married for 15 years. We have no credit card debt, and just $12,000 on a credit line we used for renovations last fall.

Our home is worth $800,000 and we have a mortgage of $214,000 at 2.9%. We have a gross annual household income of $150,000, defined benefit pensions with our employers, and invest decent amounts in TFSAs, RRSPs and RESPs for our two young kids through automated monthly deposits—though nowhere near the limits. We also donate $5,000 annually to charity.

My husband would love for us to pay off the mortgage this December with the gift money but I’m only 75% convinced. This has been a huge year of change for us, and more change may come in the next year depending on my job situation. We may move houses (to lessen my commute).

Am I being silly to put all of our money into a matrimonial home? Anything in life can happen, even when we would never expect it…

Our home is worth $800,000 and we have a mortgage of $214,000 at 2.9%. We have a gross annual household income of $150,000, defined benefit pensions with our employers, and invest decent amounts in TFSAs, RRSPs and RESPs for our two young kids through automated monthly deposits—though nowhere near the limits. We also donate $5,000 annually to charity.

My husband would love for us to pay off the mortgage this December with the gift money but I’m only 75% convinced. This has been a huge year of change for us, and more change may come in the next year depending on my job situation. We may move houses (to lessen my commute).

Am I being silly to put all of our money into a matrimonial home? Anything in life can happen, even when we would never expect it…