It’s never too late to catch up on your TFSA + MORE Jun 7th

Calculating expected returns on the sale of real estate + MORE Feb 27th

What are climate action incentive payments? + MORE Aug 14th

Minor Tweaks Won't Solve The Payday Loan Crisis + MORE Feb 22nd

The retirement reshuffle Jul 27th

The Do’s and Don’ts When Buying a Home

– ratesupermarket.ca

Buying a home is one of the most exciting yet intimidating things to do. The idea of owning your own place is thrilling, yet the prospect of having a mortgage can terrify even those who are already financial savvy. Regardless of your price range, there are some definite do’s and don’ts when buying a home.

Click here to compare mortgage rates and start saving >

It’s easy to get caught up in pictures of home décor on Pinterest, but there are some practicalities you need to consider before diving into a house hunt. Buying a home depends heavily on affordability and it should never be taken lightly.

Don’t get carried away when buying a house

Before you begin looking for a home, it’s well advised to get pre-approved for a mortgage so you have a rough idea of what you can afford. How much you’re approved for depends on a variety of factors including your income, credit history, and your down payment.

Your savings, lifestyle spending, and all the additional costs of maintaining a home need to be factored into your monthly budget says Josh Miszk, VP of Investments at Invisor…

Am I on track to retire after being laid off?

– moneysense.ca

(Photograph by Jessica Balfour)

(Photograph by Jessica Balfour)The current situation

Coleen Cudmore is single and lives in Kelowna, B.C., where, until recently, she was a manager at an insurance company. When her branch was closed in January, she received a severance package. Now, she plans to retire in December, when she turns 55, but she isn’t sure if she has enough to allow her to live on $60,000 a year. Currently, she owns a home worth $680,000 but owes $144,000 on a line of credit. She also has RRSPs and other assets worth $832,000. These investments have given her a 10% annualized return over the last few years. “I do a lot of my own investing and have a passion for it,” she says, adding that she’s been able to supplement her gross income by $500 a month using dividends from her portfolio. “It’s enough to pay the groceries,” says Cudmore, who’s using her time out of the workforce to get into a new fitness regimen. She plans to claim her CPP at age 60 and collect OAS at 65, as well as $5,400 annually from a small company pension…

7 Mostly Legal Ways To Save On Rent

– walletpop.ca

As rent prices continue to soar across Canada, here are a few ways you can take matters into your own hands and minimize your rent in the city – legally.1. Live in a ‘unique’ room*via GIPHYDoes your rental unit have a large storage room, closet or cupboard under the stairs? Could a person live in it? My sister lived in a big closet in my apartment for almost a year to save on rent. Sure it was tiny, but it fit a mattress and small side table, and for her birthday that year my roommate and I bought her a push lamp that hung on the wall. We split rent three ways (don’t worry, my sister paid less than us) and this arrangement made living downtown more affordable for all of us.2. Move in with your significant othervia GIPHYWhat used to seem like a big commitment is now just a good idea financially. It’s common sense — splitting rent, utilities and general living costs between two people is better than paying it all as one. For some people, moving in with a boyfriend or girlfriend is a huge deal, but if you’re not one of those people, why not take the leap and take advantage of the savings? Another option is to have your significant other move in with you and your roommates, or vice versa…

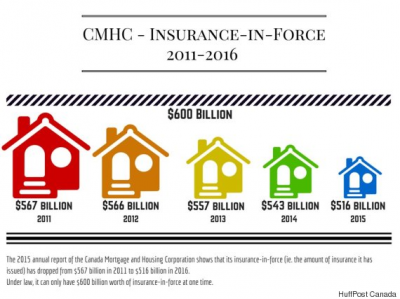

It wasn’t that long ago that the Canada Mortgage and Housing Corporation (CMHC) was reaching the limit of what it could insure in the Canadian housing market.

It wasn’t that long ago that the Canada Mortgage and Housing Corporation (CMHC) was reaching the limit of what it could insure in the Canadian housing market.

But the Crown corporation has ramped back its insurance in recent years as CEO Evan Siddall focuses on its exposure to risky housing markets across the country.

The CMHC notes in its 2015 annual report, which was released Monday, that insurance-in-force, or the amount of insurance that has been issued by the provider, stood at $526 billion last year.

That was down from $543 billion in 2014, and $557 billion in 2013.

By law, the CMHC can only have $600 billion worth of insurance issued at any one time. Insurance-in-force had been even higher before, at $567 billion in 2011 and $566 billion in 2012.

The corporation aims to have only $516 billion worth of insurance-in-force this year.

Insurance-in-force decreased in 2015 as new loans totaled $55 billion, while pay downs and loan amortizations were $72 billion.

A home for sale in Vancouver in 2010…

India seeks tycoon’s extradition, says UK nixes deportation

– canadianbusiness.com

Finance Minister Arun Jaitley says the UK will not simply deport Mallya because he entered the country on a valid passport in March, though India revoked it a month later.

Jaitley told Indian lawmakers on Wednesday that India will begin extradition proceedings once official charges are filed against the businessman.

India’s Enforcement Directorate is still gathering evidence as part of its investigation into the tycoon’s debts totalling 94 billion rupees ($1.4 billion).

The post India seeks tycoon’s extradition, says UK nixes deportation appeared first on Canadian Business – Your Source For Business News.