The bond risk many investors overlook Jul 5th

CMHC says annual pace of housing starts slowed in September Oct 10th

Latest in Mortgage News: Toronto Home Prices Set July Record Aug 9th

Buying a second home: How it works in Canada + MORE Sep 25th

Good debt and Bad debt…. do we Canadians recognize the difference? Oct 25th

Even George R.R. Martin couldn’t dream up the calamity that would befall us if Canada tightened mortgage rules.

Even George R.R. Martin couldn’t dream up the calamity that would befall us if Canada tightened mortgage rules.

That about sums up the sentiment espoused by Will Dunning, chief economist of Mortgage Professionals Canada on Tuesday.

In a stunning news release, he said that tightening lending conditions would have “tragic” consequences for the Canadian economy. He went on to say there’s “insufficient proof that a bubble exists” and that there was none of a “speculative mindset.”

Dunning also said there’s “no evidence of an increase in risk by borrowers or lenders.”

Every one of those statements flies in the face of recent expert analysis on the Canadian housing market.

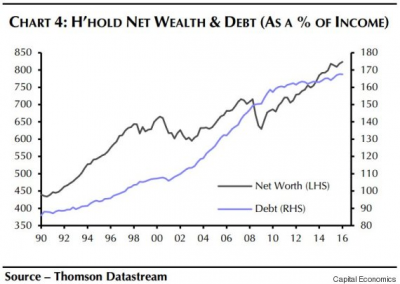

Earlier this month, Capital Economics issued a report that said Canada’s housing bubble would “end in tears.”

Economist Paul Ashworth blamed house price growth on people racking up more and more debt, a trend that was “fuelled by relaxed lending standards,” he said.

“The decline in interest rates and interest servicing costs allowed households to expand their debt without increasing the proportion of their incomes needed to meet their overall debt service obligations,” Ashworth added…

Mortgage Career: Educators’ Financial Group

– canadianmortgagetrends.com

This mortgage loophole puts us at risk

– moneysense.ca

According to their analysis the six big banks would lose nearly $12 billion while CMHC and other mortgage insurers would be on the hook for as much as $6 billion, but only if Canada were to experience a U.S.-style housing crisis where home values were to fall by as much as 35%.

Apparently, the report was a stress-test: a number-crunching exercise to reveal the worst-case scenario; situations that might occur, like a sharp increase in interest rates or massive job layoffs. But one Toronto mortgage broker is far less concerned about less than probable extreme market corrections.

The five-year fixed loophole

Based out of Toronto, Calum Ross works with high net worth clients as a dually licensed wealth advisor (with his MBA) and as an independent mortgage broker. Over the years, Ross has grown more and more concerned with mortgage qualification rules and how loopholes could contribute to over-leveraged homeowners and a potentially catastrophic future fall-out…