Learn more about Canadian mortgage rates, rules and the latest news – read on!

Latest News

2022 – Year in review Jan 3rd

As we turn the page on yet another tumultuous year, we wanted to take a look back at some of the top mortgage-related stories of 2022 and how mortgage rates fared..... More »

Making sense of the markets this week: September 24, 2023 + MORE Sep 23rd

Allan Small, Senior Investment Advisor at the Allan Small Financial Group with iA Private Wealth, shares financial headlines and offers context for Canadian investors.

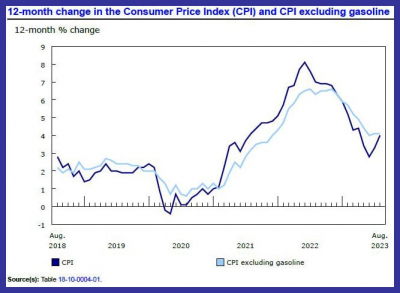

No surprise: Canada’s inflation rate ticked up in August

Canada’s annual inflation rate jumped to 4% in August, up from 3..... More »

The latest in mortgage news: Half of borrowers concerned about mortgage renewals Apr 7th

Nearly half (47%) of Canadians buying or renewing a mortgage say they are concerned about qualifying for the amount they need..... More »

The Latest in Mortgage News + MORE Jan 26th

As we do each month, we’ve rounded up some of the latest real estate and mortgage-related news from the past few weeks: Vancouver’s Housing Market Earns Dubious Honour Vancouver home prices may be falling now, but their record-high levels throughout 2018 have earned Vancouver the distinc.... More »

What is a mortgage broker? Oct 17th

Mortgage brokers are a highly regulated specialized alternative to Canada’s big banks. But what is a mortgage broker exactly? And, When it comes to the purchase of your home, why would you choose a broker over a mortgage specialist at your bank?

Get the mortgage rate that works for you.Fin.... More »

Construction at Fortress Real Developments’ LINK condominium project in Burlington in 2016 (CNW Group/Fortress Real Developments)

Construction at Fortress Real Developments’ LINK condominium project in Burlington in 2016 (CNW Group/Fortress Real Developments)Marijuana stocks and cryptocurrencies might have been the hottest speculative bets in recent months, but before that, another investment enchanted Ontario residents: syndicated mortgages. These products allow regular mom-and-pop investors to put cash into mortgages used to finance real estate developments, such as residential condo buildings. Salespeople marketed these products as fully secured, risk-free, and high-return.

Many investors have since learned those claims are not true. The promised returns have not materialized, and some of the projects attached to these loans have fallen through or have been beset by delays. Multiple lawsuits are before the courts. The provincial regulator has started issuing penalties, too. But these actions come far too late.

On Friday, the Financial Services Commission of Ontario (FSCO) issued $1.1 million in fines as part of a settlement with four mortgage brokerage companies involved with syndicated mortgages tied to real estate projects for Fortress Real Developments Inc…

Financial planning and mental illness

– moneysense.ca

Q: I am 43 with no children or spouse. I have a mental illness that is chronic and has prevented me from working and saving in my past up until the past two years.

I was able to buy a home which I converted into a duplex. I live in the walkout basement apartment while I rent the upstairs which pays the mortgage and utilities. I have $187,000 on my mortgage and I am able to work now and save $1,000 a month.

I don’t know what my future holds in terms of health and work. I am wondering if I should pay down my mortgage or invest in a TFSA mutual fund? My income is not high but I’m able to save because I’m frugal and the renters pay my mortgage.

Once my home is paid off, I can live for free and collect the rental income. What should I do with my extra $1,000 a month? My furnace is two years old and my roof is new on my home. All appliances were bought two years ago. My car is paid off and five years old.

—Elizabeth

A: Sometimes, people go about financial planning the wrong way…

Commentary: Another Regulatory Witch Hunt?

– canadianmortgagetrends.com

CMHC head Evan Siddall made a comment last fall that has credit unions worried. “CMHC will be seeking data from securitization program participants on their uninsured conventional mortgage lending,” he said. That information could result in “changes” (read, new rules) to the rulebook that approved non-federally regulated lenders—like credit unions—must abide by. Recently, I asked a […]

New mortgage rules sending borrowers to alternatives

– moneysense.ca

TORONTO — Mortgage brokers say the borrower rejection rate from large banks and traditional monoline mortgage lenders has gone up as much as 20 per cent after Canada’s banking regulator imposed a new stress test for home buyers who don’t need mortgage insurance.

As a result, alternative lenders are seeing an uptick in business as brokers increasingly direct home buyers toward borrowing options that are beyond the reach of the Office of the Superintendent of Financial Institutions’ newly enacted tighter lending requirements.

READ: Your mortgage is about to get more expensive

Clients who don’t meet the bar are turning to private lenders, mortgage investment corporations (MICs) and credit unions, which are provincially regulated and not required to implement the stress test, said Carmen Campagnaro, president of Pro Funds Mortgages in Burlington, Ont.

Campagnaro is one of the brokers who said rejected loan applications to traditional lenders have risen by 20 per cent since Jan…

As a result, alternative lenders are seeing an uptick in business as brokers increasingly direct home buyers toward borrowing options that are beyond the reach of the Office of the Superintendent of Financial Institutions’ newly enacted tighter lending requirements.

READ: Your mortgage is about to get more expensive

Clients who don’t meet the bar are turning to private lenders, mortgage investment corporations (MICs) and credit unions, which are provincially regulated and not required to implement the stress test, said Carmen Campagnaro, president of Pro Funds Mortgages in Burlington, Ont.

Campagnaro is one of the brokers who said rejected loan applications to traditional lenders have risen by 20 per cent since Jan…

Gap between housing supply and demand largest in Toronto and Vancouver: CMHC

– canadianbusiness.com

Toronto and Vancouver’s real estate markets have responded to surging prices and a growing demand for homes with a supply of new housing that is “significantly weaker than other Canadian metropolitan areas.”

The disparity between supply and demand has been largest in the two cities, but “we do not fully know why this is the case,” said the Canadian Mortgage and Housing Corporation, in a report it released Wednesday on escalating house prices in the country’s large metropolitan centres between 2010 and 2016.

Data gaps are keeping CMHC from developing a full picture of why Montreal, Calgary and Edmonton don’t have as big of an inconsistency between supply and demand as Toronto and Vancouver do, but CMHC’s deputy chief economist Aled ab Iorwerth said he has noticed Calgary and Edmonton responding to demand with “horizontal sprawl.”

As for Montreal, he said “they already have a large rental sector, there is perhaps an acceptance of living in denser housing there and they seem to be more ready to convert industrial land into housing…

The disparity between supply and demand has been largest in the two cities, but “we do not fully know why this is the case,” said the Canadian Mortgage and Housing Corporation, in a report it released Wednesday on escalating house prices in the country’s large metropolitan centres between 2010 and 2016.

Data gaps are keeping CMHC from developing a full picture of why Montreal, Calgary and Edmonton don’t have as big of an inconsistency between supply and demand as Toronto and Vancouver do, but CMHC’s deputy chief economist Aled ab Iorwerth said he has noticed Calgary and Edmonton responding to demand with “horizontal sprawl.”

As for Montreal, he said “they already have a large rental sector, there is perhaps an acceptance of living in denser housing there and they seem to be more ready to convert industrial land into housing…