Are interest payments tax deductible? Aug 12th

The Best Credit Cards for Students in 2019 + MORE May 18th

Lowest mortgage rates rise above 4% as bond yields surge Dec 12th

Canadian real estate market outlook 2018 Jan 8th

CMHC’s Gloomy Outlook: Up to 18% Drop in Home Prices, 20% Arrears Rate + MORE May 23rd

The Lender’s Equations: How Much Mortgage will you Qualify for?

– canequity.com

Monthly income generated

The amount you can contribute to your down payment

The mortgage interest rates and term you qualify for

Other financial commitments or debts you are obliged to pay

Lenders basically use two rules to determine the mortgage you are eligible to be funded to receive, in addition to examining your credit history and FICO score:

Gross Debt Service Ratio (GDS)

Total Debt Service Ratio (TDS)

The Gross Debt Service Ratio (GDS) includes mortgage payment (principal and interest), heating expenses and property tax (referred to in the mortgage industry as PITH), as well as 50 per cent of any applicable condominium fees. GDS should equate to 32 per cent* or less of your gross qualifying income.

The Total Debt Service Ratio (TDS) includes your total monthly debt obligations (vehicle payments, student loans, credit card payments, child or spousal support payments, etc…

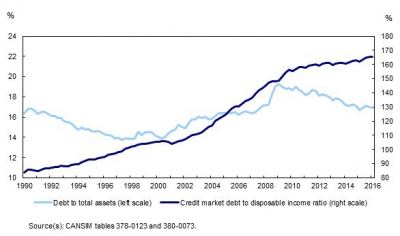

Canadians' Household Debt Avoids A New Record High, For Once

– walletpop.ca

OTTAWA — Statistics Canada says the ratio of household credit market debt to disposable income edged down in the first quarter.

OTTAWA — Statistics Canada says the ratio of household credit market debt to disposable income edged down in the first quarter.The agency says the ratio was 165.3 per cent for the first three months of 2016, down from 165.4 per cent in the fourth quarter of last year.

That means households held $1.65 in credit market debt for every dollar of disposable income.

Canadians’ household debt, as a percentage of income (dark blue line), has stabilized at very high levels. The ratio of debt to assets (light blue line) has been falling, because house prices are growing faster than total debt. (Chart: Statistics Canada)

Statistics Canada says disposable income and household credit market debt increased at nearly the same rate in the quarter.

The report also says household sector net worth rose 1.2 per cent in the first quarter to $9.633 trillion, driven by gains in the value of real estate.

Total household credit market debt, which includes consumer credit, and mortgage and non-mortgage loans, totalled $1…

Steps to getting the perfect mortgage for you

– moneysense.ca

If you’ve been saving for a home, you might be thinking now is the time to buy. Whether you’re a first time buyer or a current homeowner, buying a new home means making tough decisions. We’re here to make sure that you have a good enough understanding of mortgages before you jump right in. Here we outline the steps you need to take to make sure you get the perfect mortgage for you.

Before You Buy:

Determine the amount that you can invest in a home before you begin house hunting.

Step 1. Figure out how much to borrow:

How much you need to borrow will be determined by how much you have for your down payment and the purchase costs, such as legal fees. Ideally, try to come up with 20% of the home purchase price; otherwise, you’ll also need to factor in the cost of mortgage default insurance. You will also want to consider that your monthly mortgage payment, debt and other expenses should not exceed 40% of your income.

Need help figuring out how much you can afford? Use this mortgage calculator to get started…

Bad luck, bad advice leads to withheld tax refunds

– moneysense.ca

Q: A few years ago my wife hurt herself very badly, forcing her to take long-term disability from work. At that time, we were denied her disability payments and spent the next two years fighting for that money. But, losing her income meant we struggled to pay our bills.

Q: A few years ago my wife hurt herself very badly, forcing her to take long-term disability from work. At that time, we were denied her disability payments and spent the next two years fighting for that money. But, losing her income meant we struggled to pay our bills.Eventually, we got so behind on our mortgage payments that we put our house up for sale and I filed for a consumer proposal. We were told not to bother adding my wife. The justification is that she had no income and no other assets, so no creditors would be able to get anything from her and that meant she didn’t need creditor protection.

My consumer proposal estimated our debt at around $33,000, which included an estimate of what we’d end up owing once our house sold. The proposal was accepted by our mortgage lender and a few months later the house finally sold.

Finally, late last year, my wife won her court case and started to receive disability payments. We thought the whole ordeal was over, but then we got a letter from CMHC stating that we still owed a debt on our now-sold home and that they’d be withholding her tax refunds until she paid the debt in full…